This means that the company’s bank balance is greater than the balance reflected in the cash book. Intuit helps put more money in consumers’ and small businesses’ pockets, saving them time by eliminating work, and ensuring they have confidence in every financial decision they make. Most differences highlighted by the bank reconciliation procedure are due to timing differences as one organisation may have posted an item which the other has not. These accounts should be closed and any recurring debits or deposits should be transferred to more-active accounts. NSF stands for “Non-Sufficient Funds.” An NSF check is a check that a company tries to deposit but the payer’s bank returns it because there aren’t enough funds in the payer’s account. Check out Sheetgo for Finance and experience the benefits of automated bank reconciliation firsthand.

Why You Can Trust Finance Strategists

Bank reconciliation statements safeguard against fraud in recording banking transactions. As a result, you’ll need to deduct the amount of these checks from the balance. Such information is not available to your business immediately, so you record no entry in the business’ cash book for the above items. You will know about this only when you receive the bank statement at the end of the month. As a result, your balance as per the passbook would be less than the balance as per the cash book.

Reasons To Reconcile Bank Statements

In the past, it was common for a company to prepare the bank reconciliation after receiving the monthly bank statement and before issuing the company’s balance sheets. However, with today’s online banking a company can prepare a bank reconciliation throughout the month (as well as at the end of the month). This allows the company to verify its checking account balance more frequently and to make any necessary corrections much sooner. Cross-checking bank statements with the balance sheet at least once every month during the closing process is necessary. If the business has a high volume of transactions, reconciliations should be done more frequently. Reconciliation of bank statements is the process of comparing the transactions recorded in the company’s accounting records with the transactions listed on the bank statement.

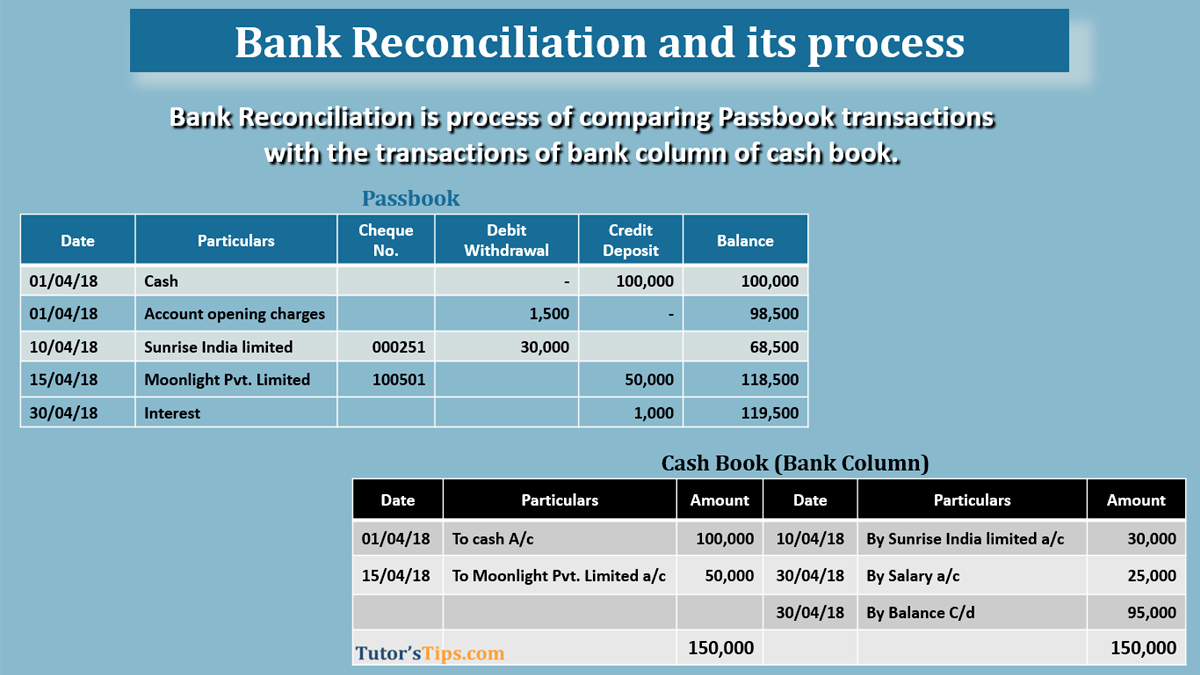

Example 1: Preparation of Bank Reconciliation Statement Without Adjusting the Cash Book Balance

Financial accuracy is also important for ensuring that all payments have been fulfilled and orders have been completed. Go through both statements and highlight any transactions that appear on only one side. Note that transactions may take a few days to clear, so the transaction date in your financial records may not precisely match the date on your bank statement. It’s recommended for a company to perform a bank reconciliation at least once a month. If your company receives bank statements more frequently, for example, every week, you may also choose to do a bank reconciliation for every statement you receive.

Free Monthly Financial Reporting Template for CFOs

Voided checks are those that should not have cleared but somehow appear as debits in your bank statement. In these cases, contact your bank to correct these errors and adjust your cash book to reflect the correct balance. Next, dive into your bank statement to find transactions not yet reflected in your company’s books. These transactions might not have been recorded in your books yet because they occurred after your last update. Non-sufficient funds (NSF) checks are recorded as an adjusted book-balance line item on the bank reconciliation statement.

We’ll explore the definition of bank reconciliation, why it’s important, and a step-by-step process for performing bank reconciliations. We’ll also look at common sources of discrepancies between financial statements and bank statements to help you identify fraud risks and errors. Performing regular bank reconciliations is key to keeping on top of your company’s financial health and paving the way for sustainable business growth. For smaller companies, it’s common to reconcile bank statements during the monthly or quarterly close process. However, there are situations where a bank reconciliation might be necessary at the earliest. For example, if a business identifies any suspicious activity or unidentifiable transactions, it’s essential to prepare a bank reconciliation immediately.

Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University.

Bank reconciliation statements are often used to catch simple errors, duplications, and accidental discrepancies. Some mistakes could adversely affect financial reporting and tax reporting. Reconcile all transactions and ensure that the closing balances match on the balance sheet and the bank statements. You only need to reconcile who should prepare a bank reconciliation? bank statements if you use the accrual method of accounting. This is to confirm that all uncleared bank transactions you recorded actually went through. When your business receives checks from its customers, these amounts are recorded immediately on the debit side of the cash book so the balance as per the cash book increases.

- Cash management software allows for scalability, making it easy to streamline the reconciliation process as the business grows.

- Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

- An online template can help guide you, but a simple spreadsheet is just as effective.

- It’s possible that a banking error has occurred or that you have been charged for something you were unaware of.

After including all the amounts identified in Step 3, your statements should display the same final balance. If any discrepancies cannot be identified and reconciled, it may signal an error or risk of fraud which your company can investigate further. Errors in the cash account result in an incorrect amount being entered or an amount being omitted from the records. The correction of the error will increase or decrease the cash account in the books. After adjusting the balances as per the bank and as per the books, the adjusted amounts should be the same.

All of this can be done by using online accounting software like QuickBooks, but if you are not using accounting software, you can use Excel to record these items. As a result of these direct payments made by the bank on your behalf, the balance as per the passbook would be less than the balance as per the cash book. After adjusting all the above items what you’ll get is the adjusted balance of the cash book.